Waiting for interest rates to come down before buying a home can be a mixed strategy, and it depends on several factors.

I wish there was a set answer, but the truth is that it all depends on your situation. In my experience, waiting for rates to decrease often proves less advantageous. If interest rates are the sole obstacle to your home purchase, it is highly likely that you will incur higher costs by postponing your decision. Instead of focusing solely on rates, let focus on what your goals are and what is most important to you. At the end of the day, you are looking for a payment that is comfortable for you & your family.

Here are some things to consider…

Pros of Waiting:

- Lower Monthly Payments: If rates decrease, you could secure a lower mortgage payment, making homeownership more affordable. A lower interest rate could allow you to afford a more expensive home without a significant increase in your monthly payment.

- Note: While this is true, you need to consider home appreciation. Homes on average appreciate 3-5% a year. That same house you were looking at; is now much more expensive & the equity that the house has now gained could have been in your pocket.

- Increased Affordability: A lower interest rate can help with qualifying for a bigger house. It can help with qualifying for different programs.

Many people hesitate to take action on interest rates based on advice from those outside the industry or by absorbing negative headlines in the news. In a later section of this blog, I’ll explain why it’s crucial to rely on the insights of professionals who truly understand the market.

Cons of Waiting:

- Market Conditions: If rates drop, it could lead to increased demand, driving home prices up. You might end up paying more for a home than you would at current rates.

- Timing Uncertainty: Predicting when rates will fall can be difficult. They could remain stable or even rise, leaving you in a less favorable position.

- Current Market: Opportunities: Depending on your local market, there may be good deals available now, even if rates are higher. Sellers may be more motivated in a less competitive market to give money at the closing table.

- Renting Costs: If you’re currently renting, rising rents could offset any savings from waiting for lower mortgage rates.

- Note: While renting offers certain advantages, if your only hesitation in purchasing a home is the interest rate, it’s important to consider the long-term implications. When you rent, you are effectively paying 100% interest, with no return on that investment. In contrast, homeownership allows you to invest in your future, providing the opportunity to recoup a portion of your expenditure. Rather than having all your funds go towards something transient, owning a home allows you to build equity and invest in yourself.

- Between 2019 – 2023, rent increased 30.4% Nationwide, while wages only increased 20%. In August of 2023, the median household spent 29.9% of their income on rent.Let’s consider a quick example: If you rent for the next five years at $1,200 a month (while the national average is around $1,500), you would end up spending $72,000 over that period—money you won’t see again. Now, let’s explore why investing that $1,200 into a home you own is a far more beneficial choice than continuing to rent.

Oh wait… I thought that was the only negatives to waiting, but here is some more.

5. Home Appreciation: Historically, homes appreciate at an average rate of 3-5% per year. This means that the property you’re considering now will likely be significantly more expensive by the time interest rates decrease.

6. Get In Line: Moreover, there is a considerable number of potential buyers waiting for rates to drop, which will create a highly competitive market once that happens. This competition may lead to bidding wars, where buyers are likely to present higher offers to secure their desired properties.

Additionally, with housing inventory already at low levels, the market will become increasingly crowded, further intensifying the competition.

Here Are Some Benefits of Buying During those “High Rates”:

- Seller Contributions: Sellers are often willing to contribute to closing costs, allowing you to minimize your out-of-pocket expenses depending on the financing program you choose. However, once interest rates decline, it’s unlikely that sellers will be as accommodating with closing cost assistance. This could mean that you’ll need to bring more cash to closing, covering both your down payment and closing costs. Additionally, you may find yourself needing to make higher offers to compete with other buyers.

- Equity Growth/Appreciation: In my opinion, purchasing now allows you to start building equity rather than waiting and potentially paying more as home values appreciate. By taking advantage of sellers willing to assist with closing costs, you can secure a favorable deal. When rates do eventually drop, you can refinance rather than entering a competitive market.

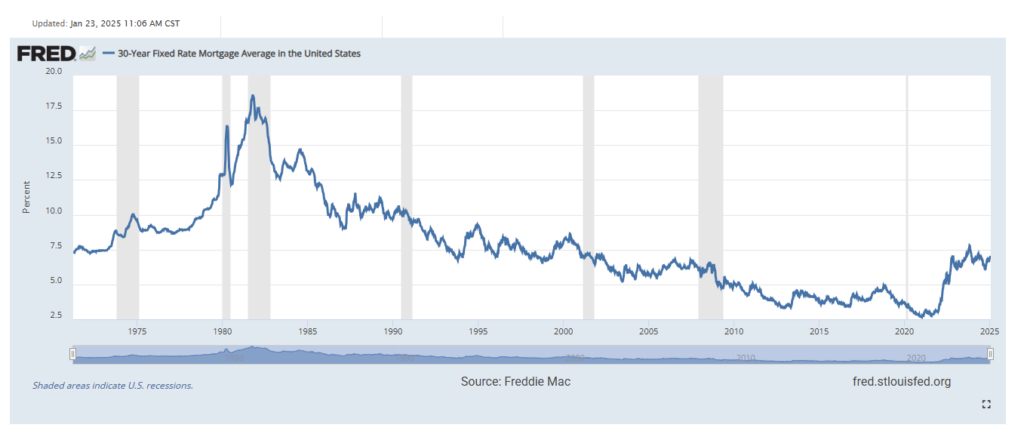

- Rates Throughout History: If you’re hoping for rates to return to the 3% range, it’s important to consider that such lows may be a long way off—potentially not occurring until we face another major economic event like a pandemic. Historically, rates in the 5-6% range are actually quite favorable. For context, mortgage rates in the 1980s and 1990s reached as high as 12-18%.

Rates Throughout History:

As you can see, the only period when interest rates dipped below 5% was following the housing crash in 2008, remaining relatively stable for the next decade. While that was an excellent time to buy, many individuals in my generation were still in middle school at the time. The lowest rates we experienced were during the COVID-19 pandemic, and it’s unlikely we’ll see those levels again without a similar economic event.

Today, rates are at their lowest point in the past two years. Don’t miss out on the opportunity to purchase a home just because your parents secured a 3% rate during a recession or pandemic. I encourage you to speak with your grandparents about their experiences with mortgage rates when they bought their homes. Additionally, consult with professionals who can provide informed advice and insights.

Freddie Mac, 30-Year Fixed Rate Mortgage Average in the United States [MORTGAGE30US], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/MORTGAGE30US, January 27, 2025.1

My Conclusion & Thoughts:

Ultimately, whether waiting is a smart move depends on your personal financial situation, local market conditions, and your readiness to buy. Consulting with a real estate professional can help you assess your options more clearly. It’s essential to balance that decision with current market conditions and your personal circumstances. Stay informed and consider consulting with a mortgage professional for tailored advice.

You can restructure your payment when rates come down, you can’t restructure your price. The supply demand imbalance isn’t going away anytime soon and when rates come down, prices are going up. Let’s find a monthly payment that fits your budget and remember this isn’t going to be the last home you buy.

Leave a Reply